There is a point in some tax-efficient investment cases where the conversation can start to sound very tidy.

The client has an inheritance tax concern.

Or an income tax liability.

Or a gain they want to manage.

Or they have used other allowances and want to know what else could be considered.

And before long, Business Relief, EIS, AIM portfolios or VCTs are part of the discussion.

That does not mean they are wrong.

Far from it.

For the right client, in the right circumstances, these can be valuable planning tools.

But they are rarely simple advice cases.

And that is where the suitability conversation needs to slow down a little.

The relief is not the whole recommendation

Tax relief is often the reason the conversation starts.

It is usually the bit the client understands first.

It can feel tangible.

It can feel attractive.

It can feel like the “why” behind the recommendation.

But it cannot do all the heavy lifting.

Because underneath the relief, there are still some fairly big advice questions.

Can the client afford the risk?

Do they understand the liquidity position?

Is the holding period realistic?

Do they understand what smaller-company exposure really means?

Could they cope if the investment falls in value?

Have simpler planning options been considered first?

And probably one of the most useful questions:

Would this still feel suitable if the tax relief was not there?

Not because the tax relief is irrelevant.

It clearly matters.

But if the recommendation only works when the tax benefit is doing most of the talking, it probably needs more challenge.

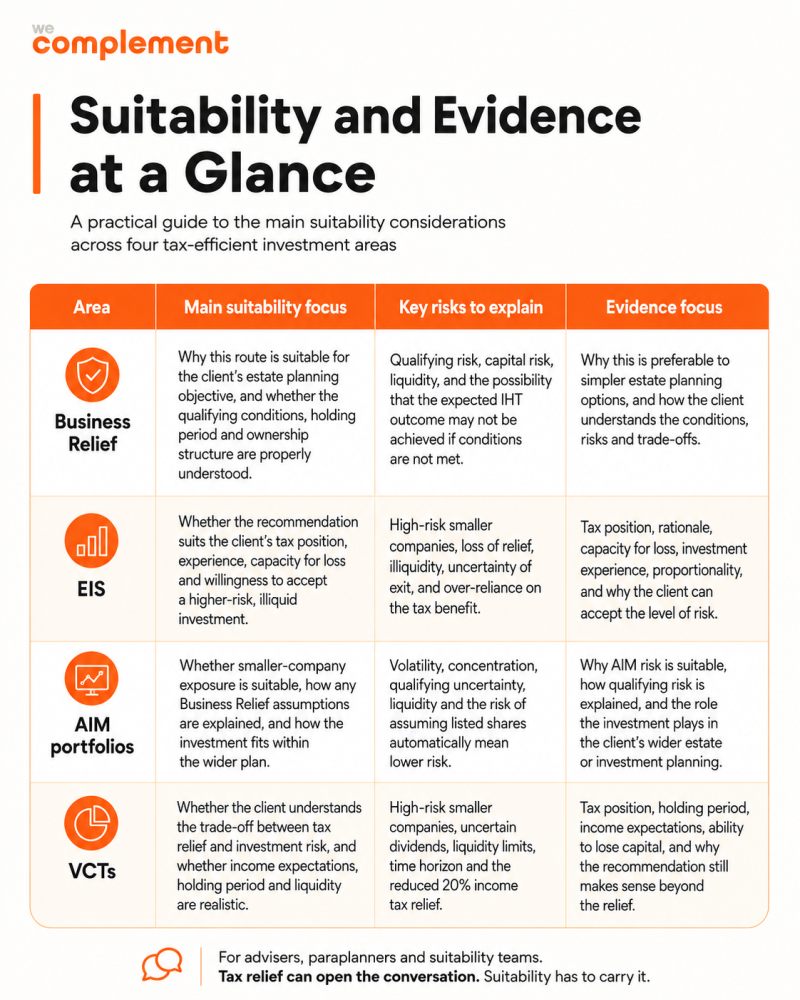

Different products, similar suitability themes

Business Relief, EIS, AIM portfolios and VCTs all do different jobs.

They have different rules, different planning uses, different risks and different client outcomes.

But when you look at the suitability work behind them, a lot of the same themes keep coming up.

Risk.

Liquidity.

Client understanding.

Capacity for loss.

Time horizon.

Charges.

Investment experience.

The client’s wider plan.

And whether the recommendation is proportionate to the objective.

That last one matters.

Because it is very easy for a tax-efficient investment to look sensible in isolation.

The harder question is whether it makes sense for this client, at this point, for this objective, with this level of risk.

Here’s a simple way to look at the main suitability focus, key risks and evidence points across four common tax-efficient investment areas.

It is not a replacement for full research or advice, but it can be a useful sense-check before the recommendation becomes too focused on the relief.

The report needs to explain the trade-off

A good suitability report should not just explain how the tax relief works.

It should explain the trade-off.

What is the client hoping to achieve?

Why is this route being considered?

What alternatives have been discounted?

What are the main risks?

How has capacity for loss been evidenced?

What does the client understand about access, holding period and potential loss?

How does this investment fit alongside the rest of the client’s planning?

That is where the advice becomes more defensible.

Not because every sentence needs to sound technical.

But because the reasoning is clear.

A reviewer should be able to follow the logic without having to guess why the recommendation was made.

And the client should be able to understand what they are accepting, not just what they might save.

A practical sense-check for advisers

Before finalising a tax-efficient investment recommendation, it can help to step back and ask:

1. What is the real planning objective?

Is this about inheritance tax planning, income tax relief, CGT deferral, tax-efficient income, portfolio planning, or something else?

And is that objective clearly evidenced in the file?

2. Is the recommendation proportionate?

Does the level of risk, complexity and illiquidity make sense compared with the client’s need?

Or is the tax benefit pulling the case further than it should?

3. What risks need to be explained clearly?

Not just listed.

Explained.

Capital risk.

Liquidity risk.

Qualifying risk.

Smaller-company exposure.

Exit risk.

Holding period.

Income uncertainty.

The client needs to understand the trade-off in plain English.

4. What would make this case hard to defend later?

This is a useful one.

If the file was reviewed in two years, what would someone question?

The client’s capacity for loss?

Their investment experience?

The size of the recommendation?

The reason simpler options were discounted?

The explanation of liquidity?

Those are often the areas worth tightening before the report is finalised.

Where the real work sits

A lot of the work behind good advice happens before the client ever sees the final report.

The research.

The challenge.

The provider and product checks.

The awkward questions.

The gaps that need filling.

The “hang on, does this actually fit?” bit.

It is not always the most visible part of the advice process.

But it is often the part that makes the recommendation stronger.

And with Business Relief, EIS, AIM portfolios and VCTs, that work really matters.

Because these recommendations need more than a tax explanation.

They need evidence that the client understands the risks, accepts the trade-off and is suitable for the route being recommended.

We have pulled together a practical guide

At We Complement, we have created a guide called:

Tax Relief Isn’t the Whole Story

It covers Business Relief, EIS, AIM portfolios and VCTs from a suitability angle.

It is not designed to be a technical tax manual or a product guide.

It is more of a practical support piece for advisers, paraplanners and suitability teams who want to sense-check the questions behind these recommendations.

Inside, we look at:

- the main suitability considerations across BR, EIS, AIM portfolios and VCTs

- the risks that need to be explained clearly

- the evidence that should sit behind the recommendation

- client understanding and capacity for loss

- how to stop the tax relief becoming the whole story

- practical questions to ask before the report is finalised

Because tax relief can open the conversation.

But suitability has to carry it.

If you would like a copy of the guide, give us a shout and we will send it over.

Useful external links

For advisers who want to check the underlying rules and guidance, these are useful places to start:

Business Relief for Inheritance Tax

Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCT) changes

These links do not replace provider due diligence, tax advice or firm-specific compliance guidance, but they are useful reference points when sense-checking the advice file.